Numerous weeks ago I took out a payday loan to help get through the pandemic

I likewise needed a payday advance because I moved back to New York from Texas with a full-time task at a telecom business, with benefits and making $17 an hour– simply enough with the right rent and cautious preparation to hardly manage in NYC 2.0, but not enough to conserve, inadequate to face any straitened scenarios. Yet here was COVID-19, as well as a bad housemate circumstance that set off a series of anxiety-causing money problems, in addition to allergies to the six felines in my home.

I started looking for a brand-new place as quickly as this all ended up being clear, but faced the normal apartment or condo search difficulties that exist in the city even without a continuous crisis– price, suitability, age discrimination– in addition to the added pressure of having no sanctuary at my home.

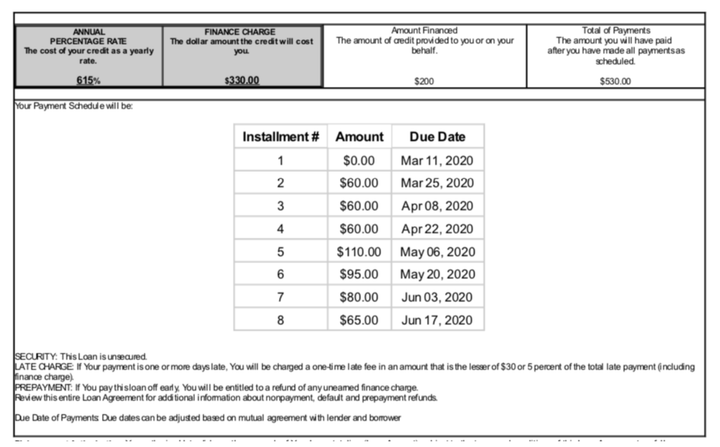

Loathe to obtain from good friends, broke from the upfront lease on the new location, completely familiar with how absolutely wrong the choice was, I pulled the trigger on a $200 loan. I currently understood the company from having actually used them throughout another jam-up a couple of years earlier.

And like me, most of the millions of other consumers who buy from the overwelming panoply of payday loan companies find themselves agreeing to astronomical terms.

If I can handle to pay it off early, I will avoid the staying finance charges, but who can pay anything off early in a pandemic? I still have to worry about real estate, task and food security.

As a previous and, therefore, “VIP” client, I was enabled to postpone my first payment, with the rest still remorselessly hoovered out the minute my paycheck is deposited.

These businesses are some of the worst predators that metastatic Late Capitalism conjures: Without tight regulation, they should not exist; much fairer alternatives have actually been proposed.

A 2019 study discovered that 40%of American households do not have the cash on hand or assets to weather three months of income crisis at poverty level. For that reason, that large portion of working Americans with typically bad-to-no credit are often forced to turn to these loans to get through the whole register of financial obligations– energy expenses, vehicle payments, medical needs– and are likewise frequently required to roll their loans over or take out brand-new loans to pay on the. This accumulate huge sums of debt that then end up being a brand-new and even worse crisis.

If I can manage to pay it off early, I will avoid the remaining finance charges, however who can pay anything off early in a pandemic? I still need to worry about housing, task and food security.

Payday/installment loan providers depend on and make the most of cognitive predispositions. One’s sense of optimism and self-control remain in play. Thanks to how the decision-making brain evolved, there’s another bias at work too: hyperbolic discounting, which picks a more instant and smaller reward (the cash) over a later and better benefit (like not having the debt).

Due to the fact that the loans have such short-terms, payment is tough; a style planned to encourage– if not requ